10 Accounting Problem Solving Skills and How To Improve Them

Discover 10 Accounting Problem Solving skills along with some of the best tips to help you improve these abilities.

Accounting is an important skill for anyone who wants to be financially successful. Without a basic understanding of accounting, it can be difficult to make sound financial decisions. However, even if you have a strong understanding of accounting principles, you may still encounter occasional accounting problems.

When these problems arise, it is important to have strong problem solving skills in order to find a resolution. In this guide, we will discuss some tips for solving accounting problems. We will also provide an overview of some common accounting problems so that you can be prepared in the event that one arises.

Financial Statements

Regulatory filings, revenue projections, account reconciliation, general ledger, business knowledge, problem solving.

Financial statements are important because they provide a snapshot of a company’s financial health. They can be used to make decisions about whether or not to invest in a company, and they can also be used to track a company’s performance over time. Financial statements include the balance sheet, income statement, and cash flow statement.

Payroll is an important skill for accountants because it allows them to process and manage employee compensation and benefits. Payroll processing includes calculating gross wages, deductions, and net wages; preparing payroll tax returns; and managing benefits such as health insurance, retirement plans, and paid time off.

Accountants who can effectively manage payroll can help businesses save time and money. They can also help businesses comply with federal and state tax laws and regulations.

Regulatory filings are important because they are required by law. Companies must file certain documents with government agencies in order to operate. These filings include tax returns, annual reports, and shareholder communications. Failure to file these documents can result in penalties or even the closure of a company.

Regulatory filings are important because they provide transparency. By law, companies must file certain documents with government agencies. These filings are public, which means that anyone can access them. This transparency allows investors and other stakeholders to see how a company is operating.

Revenue projections are important for businesses because they help businesses plan for future income. Revenue projections can be used to determine how much money a business will need to operate and grow. Revenue projections can also be used to help businesses raise money from investors.

Revenue projections are important because they help businesses plan for future income. Revenue projections can be used to determine how much money a business will need to operate and grow. Revenue projections can also be used to help businesses raise money from investors.

Account reconciliation is the process of ensuring that all transactions in a company’s books are accurate. This process is important because it helps ensure that the company’s financial statements are accurate and can be relied upon by investors, creditors and other stakeholders.

Account reconciliation involves comparing the company’s books with the records kept by its banks, vendors and other parties with whom it does business. If there are any differences, they need to be investigated and resolved. This process can be time-consuming, but it is important to ensure that the company’s books are accurate.

Compliance is the process of ensuring that you are in compliance with the laws and regulations that apply to your business. It is important for businesses to be compliant because it helps to protect them from penalties and fines. Compliance also helps to build trust with customers and regulators.

To be compliant, businesses need to understand the laws and regulations that apply to them and then take the necessary steps to ensure that they are following the rules. For example, businesses that sell products to consumers need to be aware of the consumer protection laws that apply to them. Businesses that operate in certain industries, such as healthcare, need to be aware of the regulations that apply to them.

General ledger is an important accounting problem solving skill because it is used to track and report financial information for a business. The general ledger is a summary of all of the accounts that make up the financial statements, and it is used to keep track of the money coming in and going out of the business. The general ledger is also used to prepare financial statements, and it is important that the information in the general ledger is accurate and up to date.

Quickbooks is an important skill for anyone in the accounting field. Quickbooks is a software program that helps accountants and business owners keep track of their finances. Quickbooks can help you track invoices, manage payroll, and create financial reports. Quickbooks is a valuable skill because it can save you time and make your job easier.

Business knowledge is important for accounting problem solving because it helps accountants understand the context of the problem they are trying to solve. It also helps them identify the root cause of the problem and develop a solution that will be effective in the real world.

Accounting problem solving often involves looking at a company’s financial statements and trying to identify where the company is spending too much money or where it is making mistakes in its accounting practices. To do this, accountants need to understand the company’s business and the industry in which it operates. They also need to be familiar with the latest accounting standards and best practices.

Problem solving is an important skill for accountants because they often have to solve complex problems. Problem solving requires the ability to identify the problem, gather information, develop a plan and implement the plan. Accountants must be able to think critically and creatively to solve problems.

Problem solving often requires good communication skills. Accountants must be able to explain the problem, gather information and develop a plan with the client. They also need to be able to follow up to make sure the plan is working and to troubleshoot if there are any issues.

How to Improve Your Accounting Problem Solving Skills

1. Understand the basics of accounting If you want to improve your accounting problem solving skills, it is important to have a strong foundation in accounting principles. You should be able to read and understand financial statements, as well as have a working knowledge of payroll, regulatory filings, revenue projections and account reconciliation.

2. Be well-versed in accounting software In order to be an effective problem solver, you need to be well-versed in accounting software. This will allow you to quickly and efficiently find solutions to accounting problems.

3. Stay up-to-date on accounting news and changes It is also important to stay up-to-date on accounting news and changes. This will help you anticipate problems and find solutions more quickly.

4. Be proactive in solving problems When you encounter an accounting problem, it is important to be proactive in solving it. This means taking the time to understand the problem and researching potential solutions.

5. Communicate effectively with your team When you are working on a team, it is important to communicate effectively. This means being clear about what you need from your team members and keeping them updated on your progress.

6. Be organized and efficient When solving accounting problems, it is important to be organized and efficient. This means having a system in place for tracking your progress and keeping your work area tidy.

7. Practice problem solving One of the best ways to improve your accounting problem solving skills is to practice. This can be done by working on practice problems or by taking on small projects in your personal life.

8. Seek out feedback When you are working on solving accounting problems, it is important to seek out feedback. This can be done by asking for feedback from your team members or by seeking out feedback from a mentor.

10 Linguistic Skills and How To Improve Them

10 stakeholder management skills and how to improve them, you may also be interested in..., what does a head coach do, what does a turner construction project engineer do, what does a cracker barrel associate manager do, what does a saw operator do.

Mastering Problem Definition: A Beginner’s Guide

Introduction: Problem definition is a crucial step in problem-solving processes across various domains, including accounting and finance. It involves clearly identifying and understanding the nature and scope of the problem at hand. In this guide, we will delve into the concept of problem definition, its importance, and how learners in accounting and finance can effectively apply it in their field.

Key Points:

- Definition of Problem Definition: Problem definition refers to the process of clearly articulating and understanding the problem or challenge that needs to be addressed. It involves defining the scope, boundaries, and objectives of the problem-solving endeavor.

- Clarity: Clearly defining the problem helps in avoiding ambiguity and ensures that all stakeholders have a shared understanding of the issue.

- Focus: A well-defined problem allows individuals to concentrate their efforts and resources on finding relevant solutions, leading to more effective problem-solving outcomes.

- Efficiency: By precisely defining the problem, unnecessary time and resources spent on addressing irrelevant issues can be minimized, leading to increased efficiency.

- Alignment with Goals: Problem definition ensures that the identified problem aligns with the overall goals and objectives of the organization or project.

- Identifying the Problem: The first step involves recognizing the existence of a problem or challenge that needs to be addressed. This may arise from various sources such as financial discrepancies, operational inefficiencies, or strategic concerns.

- Clarifying the Objectives: Once the problem is identified, it is essential to clarify the specific objectives that need to be achieved through problem-solving efforts. These objectives should be specific, measurable, achievable, relevant, and time-bound (SMART).

- Understanding the Context: Understanding the context surrounding the problem, including its causes, stakeholders involved, and potential implications, is vital for effective problem definition.

- Setting Boundaries: Defining the scope and boundaries of the problem helps in focusing efforts on relevant aspects and avoiding unnecessary complexities.

- Identifying the problem: Declining profitability despite consistent sales.

- Clarifying the objectives: Increase profitability by reducing operational costs or increasing revenue streams.

- Understanding the context: Analyzing factors such as increasing raw material costs, inefficient production processes, or changing market dynamics.

- Setting boundaries: Focusing on internal operational factors directly impacting profitability rather than external market fluctuations.

- Kepner, C. H., & Tregoe, B. B. (1981). The New Rational Manager. Princeton Research Press. This book provides insights into structured problem-solving methodologies, including problem definition techniques, with practical examples.

Conclusion: Problem definition is a foundational step in problem-solving processes, enabling individuals to clearly understand and address the challenges they face. By defining the problem accurately, learners in accounting and finance can streamline their problem-solving efforts, leading to more efficient and effective outcomes. Understanding the importance of problem definition and mastering its techniques is essential for success in accounting and finance.

Related Posts

Written-down value (wdv) explained for beginners.

If you’re new to finance and accounting, terms like “Written-Down Value” or WDV might sound…

Activity Sampling (Work Sampling): Unveiling Insights into Work Efficiency

Activity Sampling, also known as Work Sampling, is a method used in various industries to…

This site uses cookies, including third-party cookies, to improve your experience and deliver personalized content.

By continuing to use this website, you agree to our use of all cookies. For more information visit IMA's Cookie Policy .

Change username?

Create a new account, forgot password, sign in to myima.

Multiple Categories

Accountants as Problem Solvers

August 01, 2020

By: Linda McCann , DBA, CMA, CPA ; David Horn , CPA ; Jennifer Dosch , CMA

Managers often complain that accounting graduates aren’t prepared for today’s business environment. The complexity of our global economy and the increasing influence of, and reliance on, technology leads to practitioners and instructors questioning if undergraduate accounting programs focus on the right curriculum to prepare students for careers.

One soft skill that can help prepare accounting students for their careers is problem solving. Management accountants need to be able to work cross-functionally to solve problems and provide meaningful analyses. Many colleges, universities, and accrediting bodies in academia incorporate strategic goals requiring curriculum that facilitates problem-solving skills.

As instructors, we teach technical accounting skills by demonstrating and providing practice with accounting concepts and structured problems, which we assess via homework and exams. Teaching soft skills, such as unstructured problem solving, poses greater challenges that are more difficult to incorporate into the curriculum. How can students learn and approach unstructured problem solving?

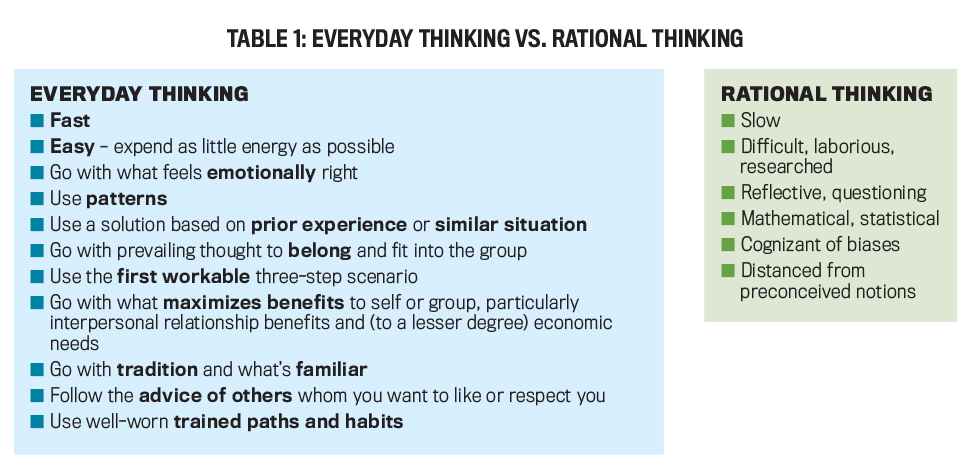

A SLOW-THINKING APPROACH

Recent scientific discoveries into the brain reveal that humans employ fast and slow thinking to solve problems. The brain especially prefers making decisions and solving problems quickly based on recognized patterns, visual and verbal cues, prior knowledge, routines, familiar preferences, prejudices, and emotions.

In contrast, decision making and problem solving often require slow thinking to digest new information, hypothesize alternatives, employ quantitative mathematical and statistical analysis, overtly recognize and break free from cognitive biases, challenge preconceived notions, synthesize ideas, and create new knowledge. To support this kind of slow, rational thinking, accountants can learn a methodical process for problem solving (see Table 1).

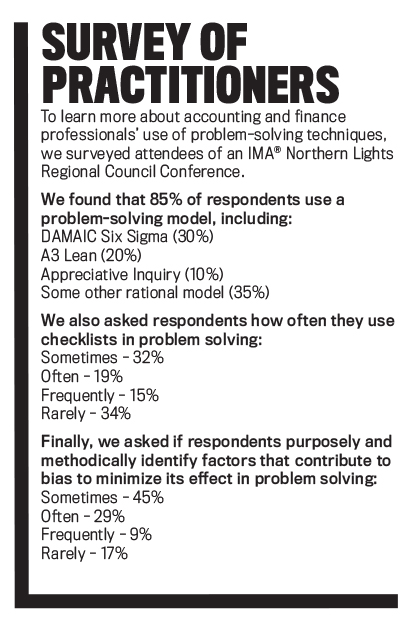

Many common business models—such as Six Sigma, A3 Lean, and Appreciative Inquiry—and the Association of American Colleges and Universities value problem solving, and critical-thinking grading rubrics describe specific steps for rational (i.e., slow thinking) problem solving. Business students, however, learn and apply these models in various courses, typically with no thread that ties them specifically to the accounting profession. Students learn bits and pieces of rational thinking throughout their undergraduate coursework, but instructors often don’t teach a common framework to apply these skills in a relevant and value-added way (see “Survey of Practitioners”).

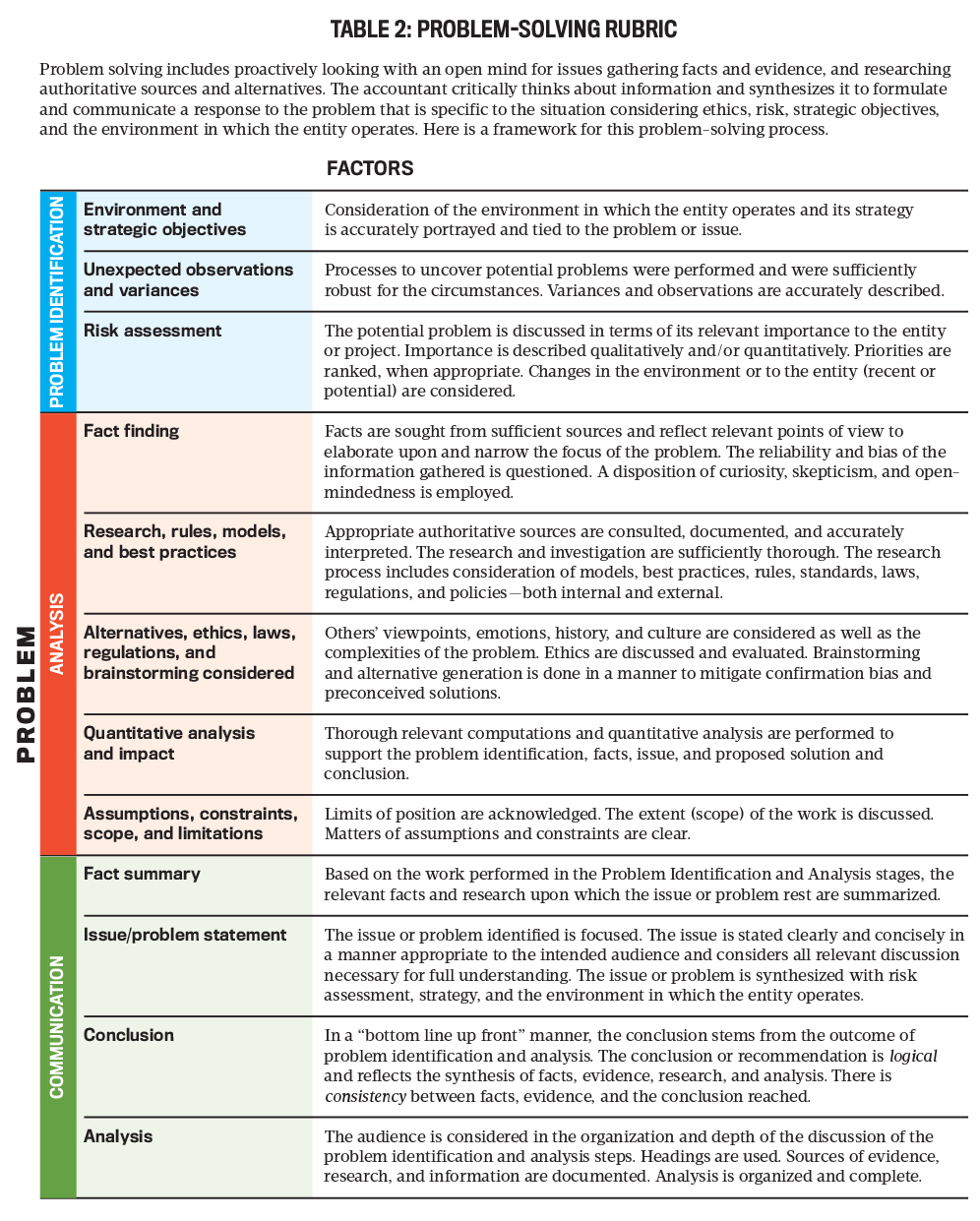

To help address this issue, we developed a problem-solving rubric for accounting students (see Table 2). The three of us are faculty members from Metropolitan State University in Minneapolis/St. Paul, Minn., and represent three different parts of the curriculum (auditing, business taxation, and management accounting), so it was important that it could be used across the entire accounting program.

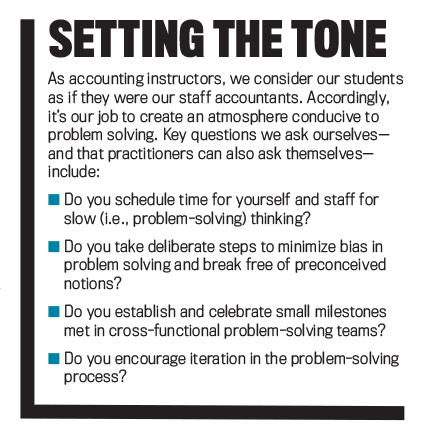

The rubric assesses learning in an organized way, providing a common framework (criteria) for students to consistently approach problem solving. The criteria include problem identification, analysis, and communication of results. It guides students through a series of problem-solving steps using terms and vocabulary specific to the accounting profession. The rubric also reminds us, as instructors, to create a learning environment where problem solving can occur (see “Setting the Tone”).

STEP 1: PROBLEM IDENTIFICATION

The iterative and looping nature of problem solving confounds inexperienced accountants. Where does one begin? Students tell us using a rubric provides a starting point.

To implement the rubric, we assign students projects with unclear goals, incomplete information, and more than one possible solution. Assignment topics vary. It could have students develop a cost-benefit analysis between adding employees or adopting Lean manufacturing techniques, analyze tax outcomes of business decisions, create a risk assessment and audit response for a fictitious client, or some other accounting-related issue.

Students begin by developing one or several hypotheses as to the nature of the problem. To generate ideas, we assist students in their brainstorming discussions. The rubric leads students to consider the environment, strategy, unexpected observations, overall importance, and risk assessment. At this stage, the identified problem may change, but the original hypothesized problem gives direction for next steps. Upon completing the assignment, we assess students on how they identified the problem.

Metropolitan State University’s business taxation course used the rubric in a case study that involves assessing the implication of the Wayfair v. South Dakota U.S. Supreme Court decision on a company’s sales tax collection. Prior to Wayfair , companies operated under a physical presence nexus established in Quill v. North Dakota . The Quill decision required companies to have a physical presence in a taxing jurisdiction in order to require collection and remittance of sales taxes on transactions.

In Wayfair , the U.S. Supreme Court overturned Quill in favor of an economic nexus standard, where companies only needed to have a certain level of economic activity. For example, in South Dakota, the threshold economic activity is 200 transactions or $100,000 in sales. The change from Quill to Wayfair was a major development in how companies operate and collect sales tax. It required companies to assess all jurisdictions in which they operate and evaluate how the change in the nexus standards impact its operations.

To apply this rubric to the change, students learn about a fictitious company that sells inventory to multiple states and collects and remits sales tax under the Quill physical presence nexus standard. We give students a subledger with all sales data for the given year. The rubric leads students to ask about implications of the Wayfair decision on the company, how the ruling impacts the company’s strategic objectives, and risks to the company because of the change in the law. Using the rubric, students are guided to discover the issue at hand, which is whether the company will have a significant number of new sales tax jurisdictions requiring collections and remittance from its customers.

Students tell us that without the rubric, they often feel like they have no road map at the beginning of a project or case study; identifying the problem seems too big and undefined to tackle. Many students initially resist engaging with unstructured problem-solving assignments because they differ from past assignments. Similar to what one might find in cross-functional teams opposed to change, students show their displeasure with crossed arms and distant body language.

Many college courses still rely on testing facts and use formulas and calculations, an approach that doesn’t put the student in the decision-making role but is familiar to them. With a rubric, students see smaller doable steps, where the assignment is heading, and how they can move forward and loop backward, when necessary. The rubric breaks down the initial intimidation students feel with unstructured problems.

STEP 2: ANALYSIS

Next, the rubric guides students through analyzing the problem using accounting-specific skills they’ve acquired in each course. For example, students consider tax laws, financial reporting and audit principles, or cost accounting techniques.

Continuing the sales and use tax example, at this stage, students apply the rubric to perform a complete analysis, enabling them to form a conclusion to communicate. What are the relevant facts to determine Wayfair ’s impact? What facts are irrelevant? What primary and secondary tax authority is needed to conduct research? Are there alternatives and exceptions to applying Wayfair ? Have all states adopted an economic nexus standard? Have all states adopted South Dakota’s transactional thresholds? What’s the quantitative impact to the company? Are there financial accounting implications to the Wayfair decision? What’s the scope of the necessary research, and are there limitations, constraints, and so on? Through the rubric, students formulate and answer questions and perform analysis to solve the problem at hand.

We assess students on their ability to gather and identify relevant facts, research any applicable rules and laws, assess alternatives, and perform any needed qualitative and quantitative analyses. At this stage, students apply theories and best practices learned in specific course fields, such as management accounting, taxation, and auditing.

To encourage elaboration, the rubric uses words such as curious, skeptical, model, assumption, authoritative, best practices, relevant, and sufficient sources. Like many accountants, students want to get their work done quickly, but problem solving takes time and slow thinking. Thanks to the rubric, more students turned in papers with greater depth, less “cut and paste,” and more relevant supporting details.

As in the real world, students often discover their original hypothesis or identified problem is incorrect, incomplete, or irrelevant. They confront the iterative nature of problem solving as they work through the analysis stage and build evidence to support their hypothesis. When evidence doesn’t support an identified problem, students go back and redefine their problem, gather new evidence, explore new alternative solutions, and build a case for their conclusion.

STEP 3: COMMUNICATION

Finally, students present their results in a memorandum to a hypothetical manager or audit partner. The memorandum mirrors common styles, such as IFRAC (issues, facts, rules, analysis, and conclusion) and BLUF (bottom line up front). Students state the problem and include the conclusion (i.e., solution) up front along with a summary of relevant facts and assumptions. Supporting documentation presents additional in-depth analysis.

This format familiarizes students with a presentation style that allows management to quickly understand conclusions while also providing more depth to support the up-front conclusion. We expect students to write and present findings in a clear and concise manner as if in a professional accounting setting. The rubric grading criteria helps students solve problems using rational thinking and delivering a memorandum that directly supports management decision making.

In the Wayfair case study, students draft a memorandum to management addressing the implications of the sales tax nexus precedence change. The facts section should discuss the company’s current sales and use tax policies. Students identify the issue as the change from physical presence nexus to economic nexus. The up-front conclusion should identify new jurisdictions from which the company needs to register and collect sales tax and quantify the volume of sales tax it expects to collect. Finally, the analysis provides an in-depth discussion of the change from Quill to Wayfair . Students should discuss how they determined new jurisdictions, limitations, and further required resources for the company.

PREPARING STUDENTS FOR THEIR CAREERS

We use the rubric format for projects or cases at different stages throughout the accounting curriculum. The problem-solving rubric measures student learning and reinforces rational thinking with each assignment. The projects that use the rubric vary in length, depth, and complexity as students move from management accounting to tax and then finally to audit. We find the rubric flexible enough to adapt to an instructor’s needs, yet it provides consistent core steps—identify the problem, analyze, and communicate—to solve problems.

The rubric helps students organize their communication through the memorandum. Setting up a memorandum so the problem and solution appear “up front” highlights mismatches between the problem, evidence, and conclusion. Further, it encourages students to decide—rather than ramble and include information that isn’t relevant. We find students often get to the communication stage and realize that their analysis doesn’t support their conclusion or identified problem. Fortunately, the rubric allows them to loop back and redefine and reanalyze.

By using the same grading criteria in multiple courses, we provide students with a familiar approach to problem solving that turns fast thinking to slow, rational thinking. The process and steps become routine and less daunting for the student. While each step still requires arduous thinking, the approach itself is a recognized pattern for students.

From our point of view as accounting instructors, the rubric helps provide consistent and fair grading. We provide separate points for milestones in problem identification, analysis, and communication, which further encourages students to go through each step of the process. Metropolitan State University plans to expand the use of this rubric in the accounting curriculum. This common framework provides students with a process to identify problems, research and investigate facts, conduct analyses, and communicate results across all accounting disciplines.

This process reinforces the problem-solving skills that students will need in their professional careers. These capabilities will help them perform their roles in today’s strategic, fast-paced business environment. Solving problems is critical for today’s management accountant. Through implementing the rubric, instructors can help students systematically apply a problem-solving process that they can take with them as they move from student to management accountant.

About the Authors

August 2020

- Strategy, Planning & Performance

- Decision Analysis

- Negotiation

- Metropolitan State University

Publication Highlights

Call for Ethics Papers: Sept. 1 Deadline

Explore more.

Copyright Footer Message

Lorem ipsum dolor sit amet

The global body for professional accountants

- Search jobs

- Find an accountant

- Technical activities

- Help & support

Can't find your location/region listed? Please visit our global website instead

- Middle East

- Cayman Islands

- Trinidad & Tobago

- Virgin Islands (British)

- United Kingdom

- Czech Republic

- United Arab Emirates

- Saudi Arabia

- State of Palestine

- Syrian Arab Republic

- South Africa

- Africa (other)

- Hong Kong SAR of China

- New Zealand

- Our qualifications

- Getting started

- Your career

- Apply to become an ACCA student

- Why choose to study ACCA?

- ACCA accountancy qualifications

- Getting started with ACCA

- ACCA Learning

- Register your interest in ACCA

- Learn why you should hire ACCA members

- Why train your staff with ACCA?

- Recruit finance staff

- Train and develop finance talent

- Approved Employer programme

- Employer support

- Resources to help your organisation stay one step ahead

- Support for Approved Learning Partners

- Becoming an ACCA Approved Learning Partner

- Tutor support

- Computer-Based Exam (CBE) centres

- Content providers

- Registered Learning Partner

- Exemption accreditation

- University partnerships

- Find tuition

- Virtual classroom support for learning partners

- Find CPD resources

- Your membership

- Member networks

- AB magazine

- Sectors and industries

- Regulation and standards

- Advocacy and mentoring

- Council, elections and AGM

- Tuition and study options

- Study support resources

- Practical experience

- Our ethics modules

- Student Accountant

- Regulation and standards for students

- Your 2024 subscription

- Completing your EPSM

- Completing your PER

- Apply for membership

- Skills webinars

- Finding a great supervisor

- Choosing the right objectives for you

- Regularly recording your PER

- The next phase of your journey

- Your future once qualified

- Mentoring and networks

- Advance e-magazine

- Affiliate video support

- About policy and insights at ACCA

- Meet the team

- Global economics

- Professional accountants - the future

- Supporting the global profession

- Download the insights app

Can't find your location listed? Please visit our global website instead

Online course

Problem solving for accountants.

As the reporting of historical performance is increasingly automated, accountants can add more value by identifying problems in organisations and proposing solutions. This involves a level of creativity that many find scary, but which we can all develop if we make the effort to do so.

This course will help you get better at identifying and solving problems in your organisation. You'll discover how to establish the root causes of problems and how you can use a variety of problem-solving techniques to develop and implement suitable solutions. The course highlights the importance of data analysis and creative thinking as well as deciding who to involve in the process. It will help you to ensure that you propose solutions that achieve the best outcomes for those affected.

This course will enable you to:

- identify and understand problems

- gather and analyse data to gain further insights into your problem and inform your proposed solutions

- unlock your creative thinking to create innovative and compelling solutions

- decide who to involve in the development of possible solutions

- assess and implement the best solutions for your organisation.

Key information

- learn at your own pace

- help meet your annual CPD requirements

- develop your own learning needs

- exclusive member benefit – 10% discount

- iPad/Android compatible

Helping accountants grow

Disclaimer: This course is available for ACCA members, you may need your ACCA membership number to complete your booking. This course and outline is provided by a third-party course provider. All course bookings are subject to the terms and conditions set by the course provider. Please see individual supplier pages for full terms and conditions. ACCA takes no liability for bookings made with third-party suppliers.

Related topics.

- Insight and business innovation

- Professional skills

- 120 days' access

- 75 GBP (exc. VAT)

- ACCA members receive 10% discount

- when using code ACCA101

Book online

You will be redirected to an external website for booking.

- ACCA Careers

- ACCA Career Navigator

- ACCA-X online courses

Useful links

- Make a payment

- ACCA Rulebook

- Work for us

- Supporting Ukraine

Using this site

- Accessibility

- Legal & copyright

- Advertising

Send us a message

Planned system updates

View our maintenance windows

What is Problem Solving? (Steps, Techniques, Examples)

By Status.net Editorial Team on May 7, 2023 — 5 minutes to read

What Is Problem Solving?

Definition and importance.

Problem solving is the process of finding solutions to obstacles or challenges you encounter in your life or work. It is a crucial skill that allows you to tackle complex situations, adapt to changes, and overcome difficulties with ease. Mastering this ability will contribute to both your personal and professional growth, leading to more successful outcomes and better decision-making.

Problem-Solving Steps

The problem-solving process typically includes the following steps:

- Identify the issue : Recognize the problem that needs to be solved.

- Analyze the situation : Examine the issue in depth, gather all relevant information, and consider any limitations or constraints that may be present.

- Generate potential solutions : Brainstorm a list of possible solutions to the issue, without immediately judging or evaluating them.

- Evaluate options : Weigh the pros and cons of each potential solution, considering factors such as feasibility, effectiveness, and potential risks.

- Select the best solution : Choose the option that best addresses the problem and aligns with your objectives.

- Implement the solution : Put the selected solution into action and monitor the results to ensure it resolves the issue.

- Review and learn : Reflect on the problem-solving process, identify any improvements or adjustments that can be made, and apply these learnings to future situations.

Defining the Problem

To start tackling a problem, first, identify and understand it. Analyzing the issue thoroughly helps to clarify its scope and nature. Ask questions to gather information and consider the problem from various angles. Some strategies to define the problem include:

- Brainstorming with others

- Asking the 5 Ws and 1 H (Who, What, When, Where, Why, and How)

- Analyzing cause and effect

- Creating a problem statement

Generating Solutions

Once the problem is clearly understood, brainstorm possible solutions. Think creatively and keep an open mind, as well as considering lessons from past experiences. Consider:

- Creating a list of potential ideas to solve the problem

- Grouping and categorizing similar solutions

- Prioritizing potential solutions based on feasibility, cost, and resources required

- Involving others to share diverse opinions and inputs

Evaluating and Selecting Solutions

Evaluate each potential solution, weighing its pros and cons. To facilitate decision-making, use techniques such as:

- SWOT analysis (Strengths, Weaknesses, Opportunities, Threats)

- Decision-making matrices

- Pros and cons lists

- Risk assessments

After evaluating, choose the most suitable solution based on effectiveness, cost, and time constraints.

Implementing and Monitoring the Solution

Implement the chosen solution and monitor its progress. Key actions include:

- Communicating the solution to relevant parties

- Setting timelines and milestones

- Assigning tasks and responsibilities

- Monitoring the solution and making adjustments as necessary

- Evaluating the effectiveness of the solution after implementation

Utilize feedback from stakeholders and consider potential improvements. Remember that problem-solving is an ongoing process that can always be refined and enhanced.

Problem-Solving Techniques

During each step, you may find it helpful to utilize various problem-solving techniques, such as:

- Brainstorming : A free-flowing, open-minded session where ideas are generated and listed without judgment, to encourage creativity and innovative thinking.

- Root cause analysis : A method that explores the underlying causes of a problem to find the most effective solution rather than addressing superficial symptoms.

- SWOT analysis : A tool used to evaluate the strengths, weaknesses, opportunities, and threats related to a problem or decision, providing a comprehensive view of the situation.

- Mind mapping : A visual technique that uses diagrams to organize and connect ideas, helping to identify patterns, relationships, and possible solutions.

Brainstorming

When facing a problem, start by conducting a brainstorming session. Gather your team and encourage an open discussion where everyone contributes ideas, no matter how outlandish they may seem. This helps you:

- Generate a diverse range of solutions

- Encourage all team members to participate

- Foster creative thinking

When brainstorming, remember to:

- Reserve judgment until the session is over

- Encourage wild ideas

- Combine and improve upon ideas

Root Cause Analysis

For effective problem-solving, identifying the root cause of the issue at hand is crucial. Try these methods:

- 5 Whys : Ask “why” five times to get to the underlying cause.

- Fishbone Diagram : Create a diagram representing the problem and break it down into categories of potential causes.

- Pareto Analysis : Determine the few most significant causes underlying the majority of problems.

SWOT Analysis

SWOT analysis helps you examine the Strengths, Weaknesses, Opportunities, and Threats related to your problem. To perform a SWOT analysis:

- List your problem’s strengths, such as relevant resources or strong partnerships.

- Identify its weaknesses, such as knowledge gaps or limited resources.

- Explore opportunities, like trends or new technologies, that could help solve the problem.

- Recognize potential threats, like competition or regulatory barriers.

SWOT analysis aids in understanding the internal and external factors affecting the problem, which can help guide your solution.

Mind Mapping

A mind map is a visual representation of your problem and potential solutions. It enables you to organize information in a structured and intuitive manner. To create a mind map:

- Write the problem in the center of a blank page.

- Draw branches from the central problem to related sub-problems or contributing factors.

- Add more branches to represent potential solutions or further ideas.

Mind mapping allows you to visually see connections between ideas and promotes creativity in problem-solving.

Examples of Problem Solving in Various Contexts

In the business world, you might encounter problems related to finances, operations, or communication. Applying problem-solving skills in these situations could look like:

- Identifying areas of improvement in your company’s financial performance and implementing cost-saving measures

- Resolving internal conflicts among team members by listening and understanding different perspectives, then proposing and negotiating solutions

- Streamlining a process for better productivity by removing redundancies, automating tasks, or re-allocating resources

In educational contexts, problem-solving can be seen in various aspects, such as:

- Addressing a gap in students’ understanding by employing diverse teaching methods to cater to different learning styles

- Developing a strategy for successful time management to balance academic responsibilities and extracurricular activities

- Seeking resources and support to provide equal opportunities for learners with special needs or disabilities

Everyday life is full of challenges that require problem-solving skills. Some examples include:

- Overcoming a personal obstacle, such as improving your fitness level, by establishing achievable goals, measuring progress, and adjusting your approach accordingly

- Navigating a new environment or city by researching your surroundings, asking for directions, or using technology like GPS to guide you

- Dealing with a sudden change, like a change in your work schedule, by assessing the situation, identifying potential impacts, and adapting your plans to accommodate the change.

- How to Resolve Employee Conflict at Work [Steps, Tips, Examples]

- How to Write Inspiring Core Values? 5 Steps with Examples

- 30 Employee Feedback Examples (Positive & Negative)

Accounting Problems (& Answers): How to Avoid Accounting Issues

Keeping up with technology and regulatory changes are significant concerns of 51% and 24%, respectively, of CPA and accounting firm survey participants, according to Accounting Today’s survey, The Year Ahead: 2022 in Numbers .

Delays in advanced software technology adoption and failures in regulatory compliance can lead to accounting challenges and problems for businesses. These accounting issues include errors in financial statements, fraud and security risks, and the potential for massive fines and imprisonment for regulatory non-compliance.

Trained business finance teams using advanced software technology that also automates regulatory compliance can overcome typical (and new) accounting problems.

What are Accounting Problems?

Accounting problems are issues resulting in material financial statement errors, undetected fraud due to inadequate internal control, misapplication of generally accepted accounting principles (GAAP accounting standards), regulatory noncompliance, and cybersecurity risks. Accounting problems may have unfavorable cash flow impacts and misstate business profitability.

What Causes Accounting Problems?

Some accounting problems are caused by using outdated software technology for accounting. Intentional fraud due to greed and poor internal control causes other financial issues. Low staffing levels can cause accounting problems. Not training the financial team causes accounting problems related to improperly applying GAAP.

The business must defend itself against cybersecurity attacks and stay up-to-date on changing regulatory compliance issues.

How do Businesses Solve Accounting Problems?

Financial professionals in businesses should use software with advanced technology capable of handling current accounting standards, including revenue recognition and lease accounting, and regulatory requirements to avoid or solve significant accounting problems.

Requiring CPA employees and accountants to take relevant continuing education courses regularly can also help businesses solve accounting problems. Adequate staffing levels help accountants solve accounting issues.

Top management must communicate an ethical tone, corporate values, employee empowerment, and key expectations.

11 Common Accounting Problems

In its fiscal year 2021, the SEC received 1,913 whistleblower complaints relating to corporate disclosures and financials, signaling possible accounting problems in these publicly-held businesses. The SEC also received whistleblower complaints related to the Foreign Corrupt Practices Act.

11 common accounting problems are:

- Revenue recognition

- Lease accounting

- Missing impairment write-downs

- Payroll errors

- Cash flow statement

- Outdated accounting software technology

- Not enough financial analysis

- Inadequate internal control

- Regulatory non-compliance

- Inadequate security

1. Revenue Recognition

Improperly applying GAAP revenue recognition standards, creating fraudulent revenue schemes, including improper accounting for consignments and third-party inventory shipments beyond the level of possible usage, and using unreasonable estimates, are revenue recognition problems.

CFODive published an article on August 20, 2020 (based on an Accounting Today analysis) titled Improper revenue recognition tops SEC fraud cases . This article highlights the significance of revenue recognition as an accounting problem.

Find an accounting software or ERP solution that helps your company achieve proper revenue recognition. Your accounting and finance teams need adequate training on FASB accounting standards to comply with GAAP revenue recognition. Excel spreadsheets are popular. But spreadsheets are error-prone and inefficient. If possible, seek a different software solution.

2. Lease Accounting

Changes to GAAP lease accounting standards require lessee companies to capitalize their operating leases with tenant right of use (ROU) and a term of over twelve months. Shorter operating leases (including office space leases) can still be recorded monthly as rent expenses. The leases are amortized over time.

Accounting standards are codified by the Financial Accounting Standards Board (FASB). Accountants must also follow other changes to the Lease accounting standard.

Business accounting teams need adequate training to follow the latest GAAP standards on Lease accounting. And they will benefit greatly by using specialized lease accounting software.

3. Impairment Write-downs and Fair Market Valuation

Accountants may miss making impairment write-downs or required adjustments for recording required assets or liabilities at a fair market valuation.

Changing economic and business conditions require accountants to periodically assess whether asset valuations have been impaired (to recognize the loss of value). Accountants must also consider adjustments to the fair value of certain assets and liabilities. Accounting professionals make adjustments through journal entries and financial statement disclosures when GAAP requires.

Supply chain backlogs and economic conditions resulting from the COVID-19 pandemic triggered accounting issues to watch for, including impairment and fair value accounting, according to EY, a top-tier accounting firm.

Examples of asset impairment include:

- Assessing goodwill from M&A transactions annually for impairment

- Considering capitalized lease asset impairment

- Recording inventory at the lower of cost or market (LCM), where market value is constrained by an upper range not exceeding net realizable value and a lower range of net realizable value less a normal profit margin.

Examples of fair market valuation include:

- Trading securities (debt and equity) held as short-term investments; gains or losses on trading securities flow to Net Income on the income statement

- Available-for-sale securities (debt and equity) held as investments to be sold before maturity; net gains or losses are included in Shareholders’ Equity as Other Comprehensive Income (Loss), listed below Retained Earnings

- Liabilities measured under ASC 820 Fair Value Measurements and Disclosures

Accountants must have adequate training to properly record asset impairments and fair market valuation when required by GAAP and make necessary financial statement disclosures. Research financial statement areas subject to accounting issues with impairment.

4. Payroll Errors

If a small business decides to calculate its own payroll, payroll taxes, and benefits, it’s possible that payment errors and accounting problems will occur. Payroll problems like miscalculating paychecks for salary expenses and hourly wages hurt employee morale and productivity.

Outsource payroll to a very experienced company providing those services, like ADP or Paychex. If the right number of hours and payroll information is provided, payments and taxes withheld should be correctly computed and compliant with tax laws. You can expect accurate reports to account for those items. Your business can make payroll tax remittances on time when due.

5. Cash Flow Statement

The cash flow statement may include errors in classification by activity type and may not include restricted cash, a newer GAAP requirement.

Cash flow statement classification errors may include misclassifying the type of activity for interest and dividends received and paid. Interest received and paid is an operating activity in the cash flow statement. Dividends received are an operating activity, and dividends paid are a financing activity in the cash flow statement.

The CPA firm, RSM, summarizes U.S. GAAP (vs IFRS) classification for certain items in the cash flow statement, including interest and dividends and restricted cash.

Cash flow statement problem solving requires keeping up to date with FASB updates and training topics related to cash flow statement preparation to understand the basics.

6. Outdated Accounting Software Technology

Outdated accounting software technology isn’t efficient, doesn’t provide real-time results for visibility in managing the company or its sales & marketing processes, relies on manual data entry and paper documents for business transaction processing and recording, and doesn’t automate regulatory compliance.

Outdated ERP systems may not be cloud-based. On-premises software systems cause inefficiencies in accessing the software and require more IT department resources to update the system and address software and hardware problems at the company’s location. These ERP systems not deployed on the cloud aren’t ideal for the changed reality of remote or hybrid work situations.

Upgrade outdated software technology in accounting software or ERP systems by changing to modern cloud-based software. If you don’t have the budget for an ERP system overhaul, consider integrating third-party add-on software to meet your needs for:

- AP automation and global mass payments software, also automating regulatory compliance

- Subscription billing (applicable to a SaaS , publishing, or utilities business model)

- Forecasting, planning, and cash management software

- Customer relationship management (CRM) software to increase efficiency and better track the sales and marketing process

- Lease accounting specialty software

- Revenue recognition software functionality, if not included in your ERP

- Data visualization software for data analytics and business intelligence

7. Not Enough Financial Analysis

An accounting team without efficient accounting systems is spending too much time closing the books, leaving less time for value-added work. Financial analysis adds value by calculating ratios, spotting and managing business trends, and providing decision support for new opportunities.

Use enhanced cloud-based ERP systems and third-party add-on software with built-in artificial intelligence/machine learning that automates accounting processes and financial analysis to the extent possible. You need real-time dashboards with your company’s KPIs (key performance indicators), including trend analysis that all functional areas with authorization privileges can access.

Supplement these systems with data visualization software like Tableau or Microsoft Power BI for data analytics with real-time capabilities and periodic automated report runs for data your company follows as timeline trends. Data visualization software embeds machine learning tools to deliver business intelligence.

8. Inadequate Internal Control

Small businesses may not have enough staffing to attain the separation of duties needed for adequate internal control. Their accounting systems may be inadequate to prevent fraud and duplicate payment errors.

When segregation of duties isn’t being achieved, get the business owner involved in the approval process as a matched vendor invoice document reviewer and second signature.

The finance and accounting department needs the human capital and software resources required to perform its duties and achieve results. Is the accounting department getting its fair share of company resources?

Custody of Assets

Custody of assets includes recorded balance sheet assets and assets not yet recorded in the books like undeposited cash.

Inventory needs controls for proper receiving, custody, secured storage with controlled access, and physical inventory in full annually and via periodic cycle counts. Office equipment should also be tagged upon receipt and subject to a physical inventory. As stated earlier, inventory should be tested for any loss in value requiring a write-down.

Discrepancies in the balance of fixed assets may result from a physical fixed asset count. Set a proper cutoff for recording fixed asset purchases.

If a fixed asset isn’t recorded, look for the purchase documents and invoice to record it. If another fixed asset isn’t counted, investigate where it may be or if it was sold. For accounting purposes, record the difference between the book value of fixed assets net of accumulated depreciation and sale proceeds, computing gain or loss on the sale of fixed assets. Write off missing fixed assets if necessary after your investigation.

Fraud, including embezzlement, may result from inadequate internal control and employee collusion.

Use modern cloud-based automation software that helps you find fraud and errors like duplicate payments. Use variance analysis and followup on significant differences for budget vs actual expenses. Review vendor master files, perform 3-way document matching for invoices, and validate vendors for authenticity before paying them.

Strive to achieve adequate segregation of duties with employee task assignments. Control or custody of assets and recording transactions in the books need to be performed by different employees.

10. Regulatory Non-Compliance

Regulatory compliance covers different areas, including taxation, data privacy and security, sanctions lists like OFAC, and the Foreign Corrupt Practices Act (FCPA).

The Foreign Corrupt Practices Act covers not making bribes in foreign countries. And the FCPA’s scope goes far beyond preventing bribes.

Violations of the Foreign Corrupt Practices Act and other regulations could result in:

- Massive fines for companies and convicted individuals

- Imprisonment

- Tarnishing a company’s and convicted individual’s business reputation and ethics

Familiarize your company, including the financial and accounting staff, with regulatory issues applying to your industry and company. Perform a project to document regulatory concerns and distribute the results widely. Hold a training session for company employees. Emphasize company values that include being ethical and empowering employees to act as the “conscience of the company.”

Find an automation software solution handling regulatory compliance. Tipalti AP automation software includes automated regulatory compliance features.

11. Inadequate Security

Cybersecurity is a significant issue that can compromise business intellectual property and customer data and employee records in your system.

Implement the most advanced cybersecurity software. Create and distribute an up-to-date company policy on required steps for achieving adequate cybersecurity. Train employees on how to avoid email and other scans that can result in hacks compromising company security.

Using Automation to Solve Accounting Problems

You can solve some accounting problems and become more efficient by applying accounting automation software. AP automation will provide significant benefits for your business.

Accounting Automation Software Applications

Businesses can deploy accounting automation in several areas to improve accounting processes and results. Accounting systems automation includes efficient financial technology (FinTech) applied to vendor invoice processing and payments and customer billing and accounts receivable.

Automate subscription billing, if applicable to your business model. Use automated customer credit decision solutions to decide which customers will be offered accounts receivable instead of requiring cash payments upfront.

Integrate CRM and marketing automation software like Salesforce and Marketo to improve sales & marketing processes and convert more new customers.

Automate forecasting, budgeting, business planning, and cash flow management.

AP Automation Software Benefits

Gain time to perform financial analysis by closing the books sooner. You can accomplish this by automating routine accounting processes like accounts payable and global mass payments with add-on AP automation software accessed via ERP integration.

Automated systems provide outsized benefits in the areas of payables automation and global mass payments to suppliers, vendors, and payouts to independent contractors, including freelancers and affiliates, and royalty recipients. Automated systems improve cash flow . They increase efficiency to let your company process vendor invoices and pay in time to take lucrative early payment discounts .

The best add-on AP automation and global mass payments software:

- Automates supplier onboarding and tax compliance

- Scans with OCR technology or uploads invoices and supporting documents electronically

- Improves your company’s expense management

- Makes efficient batch payments using a choice of payment methods

- Automates payments reconciliation and adds more accounts payable reports

- Lets your company close its books faster during the accounting cycle

- Reduces fraud and errors

- Automates regulatory compliance

Using electronic documents instead of paper-based documents:

- Ends paper-based data entry, invoice matching, and processing costs

- Creates a relevant document repository through the supplier portal

- Creates an audit trail

- Enables automatic approvals with notifications and follow-up

- Makes efficient batch payments (or single payments)

- Ends the inefficient, unsafe, and costly use of paper checks

- Automatically reconciles batch payments

The level of resources required in accounting and bookkeeping can be leveraged by efficiencies provided by AP automation software. Efficiency is improved by up to 80%. Books are closed much more quickly, letting the finance team spend more time on value-added financial analysis and decision support.

Cloud-based AP automation software using AI/ML and RPA and tools for regulatory compliance work in combination with ERP systems.

Real-time SaaS automation software and ERP systems with modern technology can prevent or solve several types of accounting problems and issues, including fraud, accounting errors related to vendor invoices and payments, GAAP compliance in financial reporting, and regulatory compliance.

And adequate training of the finance and accounting team prevents or solves accounting problems.

About the Author

Barbara Cook

RELATED ARTICLES

- PRO Courses Guides New Tech Help Pro Expert Videos About wikiHow Pro Upgrade Sign In

- EDIT Edit this Article

- EXPLORE Tech Help Pro About Us Random Article Quizzes Request a New Article Community Dashboard This Or That Game Happiness Hub Popular Categories Arts and Entertainment Artwork Books Movies Computers and Electronics Computers Phone Skills Technology Hacks Health Men's Health Mental Health Women's Health Relationships Dating Love Relationship Issues Hobbies and Crafts Crafts Drawing Games Education & Communication Communication Skills Personal Development Studying Personal Care and Style Fashion Hair Care Personal Hygiene Youth Personal Care School Stuff Dating All Categories Arts and Entertainment Finance and Business Home and Garden Relationship Quizzes Cars & Other Vehicles Food and Entertaining Personal Care and Style Sports and Fitness Computers and Electronics Health Pets and Animals Travel Education & Communication Hobbies and Crafts Philosophy and Religion Work World Family Life Holidays and Traditions Relationships Youth

- Browse Articles

- Learn Something New

- Quizzes Hot

- Happiness Hub

- This Or That Game

- Train Your Brain

- Explore More

- Support wikiHow

- About wikiHow

- Log in / Sign up

- Education and Communications

- Personal Development

- Problem Solving

How to Improve Problem Solving Skills

Last Updated: July 24, 2024 Fact Checked

This article was co-authored by Erin Conlon, PCC, JD . Erin Conlon is an Executive Life Coach, the Founder of Erin Conlon Coaching, and the host of the podcast "This is Not Advice." She specializes in aiding leaders and executives to thrive in their career and personal lives. In addition to her private coaching practice, she teaches and trains coaches and develops and revises training materials to be more diverse, equitable, and inclusive. She holds a BA in Communications and History and a JD from The University of Michigan. Erin is a Professional Certified Coach with The International Coaching Federation. There are 11 references cited in this article, which can be found at the bottom of the page. This article has been fact-checked, ensuring the accuracy of any cited facts and confirming the authority of its sources. This article has been viewed 239,734 times.

The ability to solve problems applies to more than just mathematics homework. Analytical thinking and problem-solving skills are a part of many jobs, ranging from accounting and computer programming to detective work and even creative occupations like art, acting, and writing. While individual problems vary, there are certain general approaches to problem-solving like the one first proposed by mathematician George Polya in 1945. By following his principles of understanding the problem, devising a plan, carrying out the plan, and looking back, you can improve your problem-solving and tackle any issue systematically.

Define the problem clearly.

- Try to formulate questions. Say that as a student you have very little money and want to find an effective solution. What is at issue? Is it one of income – are you not making enough money? Is it one of over-spending? Or perhaps you have run into unexpected expenses or your financial situation has changed?

State your objective.

- Say that your problem is still money. What is your goal? Perhaps you never have enough to go out on the weekend and have fun at the movies or a club. You decide that your goal is to have more spending cash. Good! With a clear goal, you have better defined the problem.

Gather information systematically.

- To solve your money shortage, for example, you would want to get as detailed a picture of your financial situation as possible. Collect data through your latest bank statements and to talk to a bank teller. Track your earnings and spending habits in a notebook, and then create a spreadsheet or chart to show your income alongside your expenditures.

Analyze information.

- Say you have now collected all your bank statements. Look at them. When, how, and from where is your money coming? Where, when, and how are you spending it? What is the overall pattern of your finances? Do you have a net surplus or deficit? Are there any unexplained items?

Generate possible solutions.

- Your problem is a lack of money. Your goal is to have more spending cash. What are your options? Without evaluating them, come up with possible options. Perhaps you can acquire more money by getting a part-time job or by taking out a student loan. On the other hand, you might try to save by cutting your spending or by lowering other costs.

- Divide and conquer. Break the problem into smaller problems and brainstorm solutions for them separately, one by one.

- Use analogies and similarities. Try to find a resemblance with a previously solved or common problem. If you can find commonalities between your situation and one you've dealt with before, you may be able to adapt some of the solutions for use now.

Evaluate the solutions and choose.

- How can you raise money? Look at expenditures – you aren’t spending much outside of basic needs like tuition, food, and housing. Can you cut costs in other ways like finding a roommate to split rent? Can you afford to take a student loan just to have fun on the weekend? Can you spare time from your studies to work part-time?

- Each solution will produce its own set of circumstances that need evaluation. Run projections. Your money problem will require you to draw up budgets. But it will also take personal consideration. For example, can you cut back on basic things like food or housing? Are you willing to prioritize money over school or to take on debt?

Implement a solution.

- You decide to cut costs, because you were unwilling to take on debt, to divert time away from school, or to live with a roommate. You draw up a detailed budget, cutting a few dollars here and there, and commit to a month-long trial.

Review and evaluate the outcome.

- The results of your trial are mixed. On one hand, you have saved enough during the month for fun weekend activities. But there are new problems. You find that you must choose between spending cash and buying basics like food. You also need a new pair of shoes but can’t afford it, according to your budget. You may need to a different solution.

Adjust if necessary.

- After a month, you decide to abandon your first budget and to look for part-time work. You find a work-study job on campus. Making a new budget, you now have extra money without taking too much time away from your studies. You may have an effective solution.

Do regular mental exercises.

- Word games work great. In a game like “Split Words,” for example, you have to match word fragments to form words under a given theme like “philosophy.” In the game, “Tower of Babel,” you will need to memorize and then match words in a foreign language to the proper picture.

- Mathematical games will also put your problem solving to the test. Whether it be number or word problems, you will have to activate the parts of your brain that analyze information. For instance: “James is half as old now as he will be when he is 60 years older than he was six years before he was half as old as he is now. How old will James be when his age is twice what it was 10 years after he was half his current age?”

Play video games.

- Play something that will force you to think strategically or analytically. Try a puzzle game like Tetris. Or, perhaps you would rather prefer a role-playing or strategy game. In that case, something like “Civilization” or “Sim-City” might suit you better.

Take up a hobby.

- Web design, software programming, jigsaw puzzles, Sudoku, and chess are also hobbies that will force you to think strategically and systematically. Any of these will help you improve your overall problem solving.

Expert Q&A

You Might Also Like

- ↑ https://www.healthywa.wa.gov.au/Articles/N_R/Problem-solving

- ↑ https://asq.org/quality-resources/problem-solving

- ↑ https://ctb.ku.edu/en/table-of-contents/evaluate/evaluate-community-interventions/collect-analyze-data/main

- ↑ https://www.mindtools.com/pages/article/newCT_96.htm

- ↑ https://www.skillsyouneed.com/ips/problem-solving.html

- ↑ Erin Conlon, PCC, JD. Executive Life Coach. Expert Interview. 31 August 2021.

- ↑ https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5930973/

- ↑ https://www.theguardian.com/lifeandstyle/2018/oct/13/mental-exercises-to-keep-your-brain-sharp

- ↑ https://www.apa.org/monitor/2014/02/video-game

- ↑ https://www.nature.com/articles/d41586-018-05449-7

About This Article

To improve your problem-solving skills, start by clearly defining the problem and your objective or goal. Next, gather as much information as you can about the problem and organize the data by rewording, condensing, or summarizing it. Then, analyze the information you've gathered, looking for important links, patterns, and relationships in the data. Finally, brainstorm possible solutions, evaluate the solutions, and choose one to implement. For tips on implementing solutions successfully, read on! Did this summary help you? Yes No

- Send fan mail to authors

Reader Success Stories

Georgia Williams

Mar 10, 2023

Did this article help you?

Mar 8, 2017

Alexis Stevens

Sep 23, 2016

Featured Articles

Trending Articles

Watch Articles

- Terms of Use

- Privacy Policy

- Do Not Sell or Share My Info

- Not Selling Info

Get all the best how-tos!

Sign up for wikiHow's weekly email newsletter

Home » Explanations » Introduction to financial accounting » Accounting equation

Accounting equation

Accounting equation describes that the total value of assets of a business entity is always equal to its liabilities plus owner’s equity. This equation is the foundation of modern double entry system of accounting being used by small proprietors to large multinational corporations. Other names used for this equation are balance sheet equation and fundamental or basic accounting equation.

Definition and explanation

We know that every business holds some properties known as assets. The claims to the assets owned by a business entity are primarily divided into two types – the claims of creditors and the claims of owner of the business. In accounting, the claims of creditors are referred to as liabilities and the claims of owner are referred to as owner’s equity.

Accounting equation is simply an expression of the relationship among assets, liabilities and owner’s equity in a business. The general form of this equation is presented below:

Assets = Liabilities + Owner’s Equity

Notice that the left hand side (also known as assets side) of the equation shows the resources owned by the business and the right hand side (also known as equity side) shows the sources of funds used to acquire these resources. All assets owned by a business are acquired with the funds supplied either by creditors or by owner(s). In other words, we can say that the value of assets in a business is always equal to the sum of the value of liabilities and owner’s equity. The total dollar amounts of two sides of accounting equation are always equal because they represent two different views of the same thing.

In accounting equation, the liabilities are normally placed before owner’s equity because the rights of creditors are always given a priority over the rights of owners. Because of this preference, the liabilities are sometime transposed to the left side which results in the following form of accounting equation:

Assets – Liabilities = Owner’s Equity

If dollar amounts of any two of the three elements are known, we can solve the equation to find the third one. For example, if a business owns total assets amounting to $400,000 and total liabilities amounting to $120,000, the owners equity must be equal to $280,000 as computed below:

Assets – Liabilities = Owner’s Equity $400,000 – $120,000 = $280,000

Using the concept of accounting equation, compute missing figures from the following:

- Assets = $100,000, Liabilities = $40,000, Owner’s equity = ?

- Assets = ?, Liabilities = $20,000, Owner’s equity = $30,000

- Assets = $120,000, Liabilities = ?, Owner’s equity = $80,000

- Assets = ?, Liabilities + Owner’s equity = $300,000

- Owner’s equity = Assets – Liabilities = $100,000 – $40,000 = $60,000

- Assets = Liabilities + Owner’s equity = $20,000 + $30,000 = $50,000

- Liabilities = Assets – Owner’s equity = $120,000 – $80,000 = $40,000

- The basic accounting equation is: Assets = Liabilities + Owner’s equity. Therefore, If liabilities plus owner’s equity is equal to $300,000, then the total assets must also be equal to $300,000.

Impact of transactions on accounting equation

Valid financial transactions always result in a balanced accounting equation which is the fundamental characteristic of double entry accounting (i.e., every debit has a corresponding credit).

Every transaction impacts accounting equation in terms of dollar amounts but the equation as a whole always remains in balance. Any increase in one side is balanced either by a corresponding decrease in the same side or by a corresponding increase in the other side and any decrease is balanced either by a corresponding increase in the same side or by a corresponding decrease in the other side. For better explanation, consider the impact of twelve transactions included in the following example:

Mr. John started a T-shirts business to be known as “John T-shirts”. He performed following transactions during the first month of operations:

- Mr. John invested a capital of $15,000 into his business.

- Acquired a building for $5,000 cash for business use.

- Bought furniture for $1,500 cash for business use.

- Purchased T-shirts from a manufacturer for $3,000 cash.

- Sold T- shirts for $1,000 cash, the cost of those T-shirts were $700.

- Purchased T-shirts for $2,000 on credit.

- Sold T-shirts for $800 on credit, the cost of those shirts were $550.

- Paid $1,000 cash to his payables.

- Collected $800 cash from his receivables.

- The shirts costing $100 were stolen by someone.

- Mr. John paid $150 cash for telephone bill.

- Borrowed money amounting to $5,000 from City Bank for business purpose.

Required: Explain how each of the above transactions impacts the accounting equation of John T-shirts.

Transaction 1: The investment of capital by John is the first transaction of John T-shirts which creates very initial accounting equation of the business. At this point, the cash is the only asset of business and owner has the sole claim to this asset. Therefore, the equation would look like the following:

Equation element(s) impacted as a result of transaction 1: “Assets” & “Owner’s equity”.

Transaction 2: The second transaction is the purchase of building which brings two changes. First, it reduces cash by $5,000 and second, the building valuing $5,000 comes into the business. In other words, cash amounting to $5,000 is converted into building. The impact of this transaction on accounting equation is shown below:

Equation element(s) impacted as a result of transaction 2: “Assets”

Transaction 3: The impact of this transaction is similar to that of transaction number 2. Cash goes out of and furniture comes in to the business. On asset side, The reduction of $1,500 in cash is balanced by the addition of furniture with a value of $1,500.

Equation element(s) impacted as a result of transaction 3: “Assets”

Transaction 4: The impact of this transaction is similar to transactions 2 and 3. One asset (i.e, cash) goes out and another asset (i.e, inventory) comes in. The cash would decrease by $3,000 and at the same time the inventory valuing $3,000 would be recorded on the asset side.

Equation element(s) impacted as a result of transaction 4: “Assets”

Transaction 5: In this transaction, shirts costing $700 are sold for $1,000 cash. It increases cash by $1,000 and reduces inventory by $700. The difference of $300 is the profit of the business that would be added to the capital. The whole impact of this transaction on accounting equation is shown below:

Equation element(s) impacted as a result of transaction 5: “Assets” & “Owner’s equity”

Transaction 6: In this transaction, T-shirts costing $2,000 are purchased on credit. It increases inventory on asset side and creates a liability of $2,000 known as accounts payable (abbreviated as A/C P.A) on the equity side of the equation. Since it is a credit transaction, it has no impact on cash.

Equation element(s) impacted as a result of transaction 6: “Assets” & “liabilities”

Transaction 7: In this transaction, the business sells T-shirts costing $550 for $800 on credit. It reduces inventory by $550 and creates a new asset known as accounts receivable (abbreviated as A/C R.A) valuing $800. The difference of $250 is profit of the business and would be added to capital under the head owner’s equity.

Equation element(s) impacted as a result of transaction 7: “Assets” & “Owner’s equity”

Transaction 8: In this transaction, business pays cash amounting to $1,000 for a previous credit purchase. It will reduce cash and accounts payable liability both with $1,000.

Equation element(s) impacted as a result of transaction 8: “Assets” & “Liabilities”

Transaction 9: In this transaction, the business collects cash amounting to $800 for a previous credit sale. On asset side, it increases cash by $800 and reduces accounts receivable by the same amount.

Equation element(s) impacted as a result of transaction 9: “Assets”

Transaction 10: The loss of shirts by theft reduces inventory on asset side and capital on equity side both by $100. All expenses and losses reduce owner’s equity or capital.

Equation element(s) impacted as a result of transaction 10: “Assets” & “Owner’s equity”

Transaction 11: The payment of telephone and electricity bills are business expenses that reduce cash on asset side and capital on equity side both by $150.

Equation element(s) impacted as a result of transaction 11: “Assets” & “Owner’s equity”

Transaction 12: The loan is a liability because the John T-shirts will have to repay it to the City Bank. This transaction increases cash by $5,000 on asset side and creates a “bank loan” liability of $5,000 on equity side.

Equation element(s) impacted as a result of transaction 12: “Assets” & “Liabilities”

In above example, we have observed the impact of twelve different transactions on accounting equation. Notice that each transaction changes the dollar value of at least one of the basic elements of equation (i.e., assets, liabilities and owner’s equity) but the equation as a whole does not lose its balance.

it was bit challenging but knowledge obtained.

This is nasir,please give me more questions and let me practice on it. Topic : accounting equatin

Excellent, I am so thankful for these explainations

It is informative and well presented. I need more examples.

I love this

Good explantions with examples, thanks buddy

Hi. I am a G11 student in this upcoming school year, thank you for the examples and a good explanation. I understand the topic more examples please.

Leave a comment Cancel reply

Accounting Equation Problems and Solutions with Examples

What is the Accounting Equation?

The Accounting Equation is based on the double entry accounting, which says that every transaction has two aspects, debit and credit, and for every debit there is equal and opposite credit. It helps to prepare a balance sheet, so it is also called the Balance Sheet Equation.

Accounting Equation Formula